geeky NEWS: Navigating the New Age of Cutting-Edge Technology in AI, Robotics, Space, and the latest tech Gadgets

As a passionate tech blogger and vlogger, I specialize in four exciting areas: AI, robotics, space, and the latest gadgets. Drawing on my extensive experience working at tech giants like Google and Qualcomm, I bring a unique perspective to my coverage. My portfolio combines critical analysis and infectious enthusiasm to keep tech enthusiasts informed and excited about the future of technology innovation.

AI in 2025: Smaller, Cheaper, and Everywhere - What Stanford's Latest Report Reveals

Updated: April 19 2025 09:16

The 2025 HAI AI Index Report, released earlier this month, paints a fascinating picture of an AI landscape that's simultaneously maturing and accelerating in unexpected ways. Let's dive into the most significant findings and what they mean for businesses, developers, and consumers alike.

The Rise of the Small but Mighty Models

Remember when bigger always meant better in AI? Those days are officially over. The 2025 AI Index provides compelling evidence that the industry's focus has shifted dramatically toward optimization.

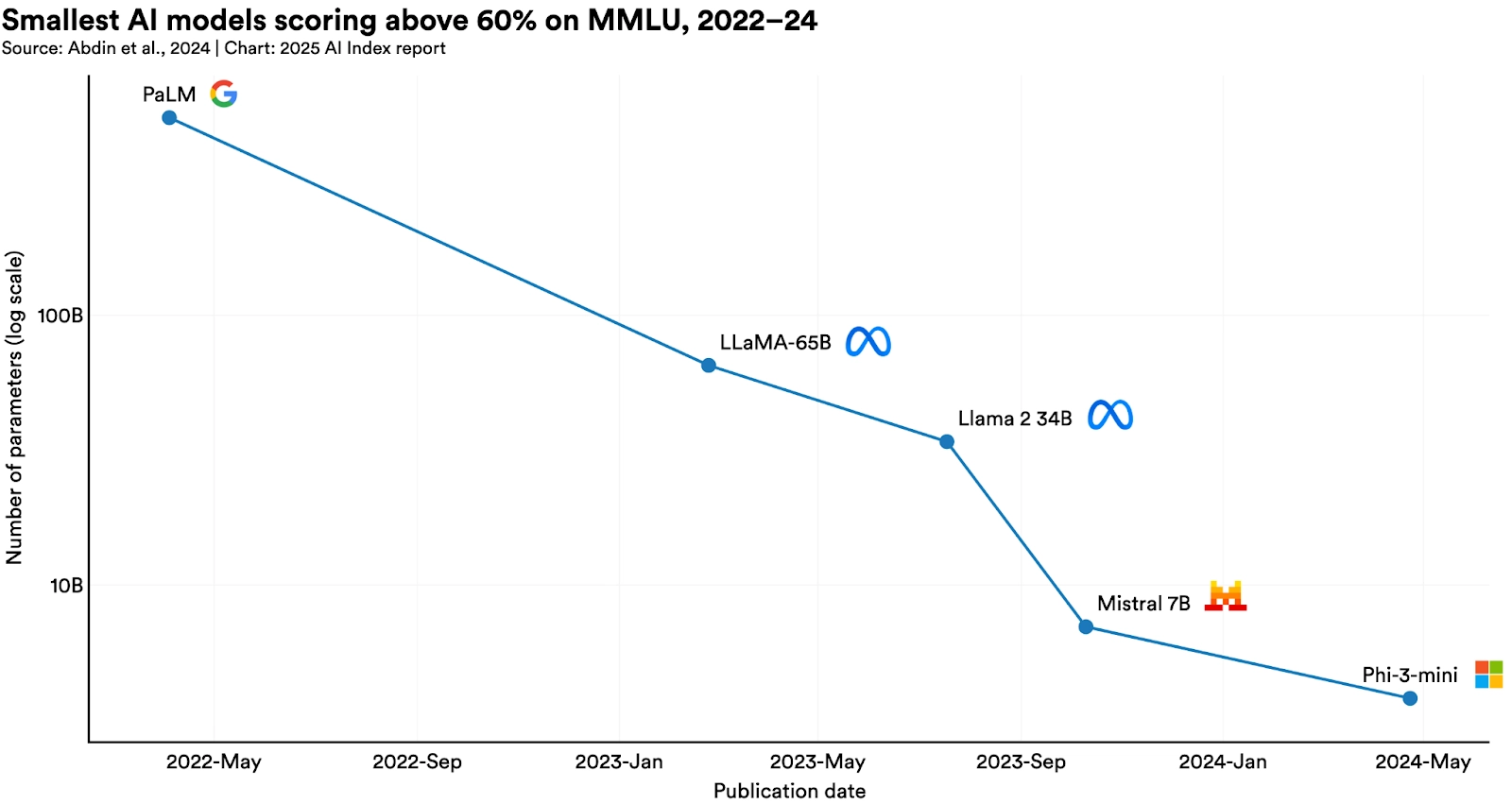

In 2022, you needed a behemoth like PaLM with its 540 billion parameters to achieve 60% accuracy on the MMLU benchmark (a key test of an AI's general knowledge and reasoning). Fast forward to 2024, and Microsoft's Phi-3-mini accomplishes the same feat with just 3.8 billion parameters.

That's a staggering 142-fold reduction in model size while maintaining equivalent capabilities. This trend isn't just academically interesting—it's revolutionizing how AI gets deployed:

Smaller models run efficiently on consumer devices

Less computational overhead means lower carbon footprints

More organizations can afford to deploy and customize models

For developers, this means AI capabilities that once required massive cloud infrastructure can now potentially run on smartphones, IoT devices, and edge computing platforms.

AI Economics: The Great Deflationary Force

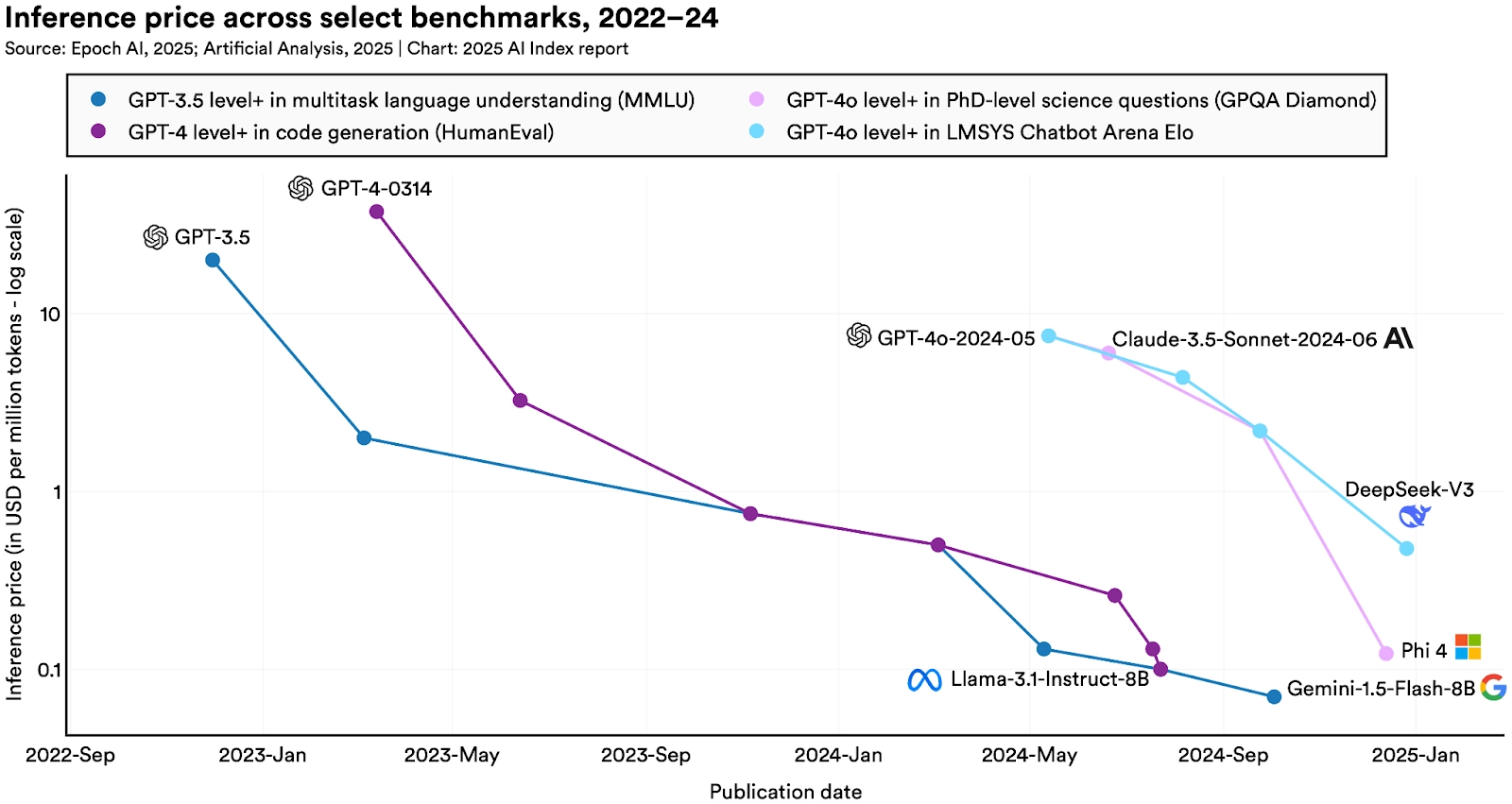

Perhaps the most dramatic statistic in the entire report relates to cost. Using an AI model with GPT-3.5-level capabilities (64.8% accuracy on MMLU) has become 280 times cheaper in just 18 months.

In late 2022, querying such a model would cost approximately $20 per million tokens. By October 2024, Gemini-1.5-Flash-8B offered equivalent performance for just $0.07 per million tokens.

This price collapse isn't uniform across all AI tasks—the report notes that depending on specific applications, costs have fallen anywhere from 9 to 900 times annually. But the trend is unmistakable: AI is experiencing a deflationary pricing curve steeper than almost any technology in history.

The economic implications are profound. AI capabilities that were prohibitively expensive for most businesses just two years ago are now accessible even to small startups and individual developers. This democratization of access will likely accelerate AI adoption across sectors that have been slow to embrace the technology.

The Global AI Race: China's Rapid Ascent

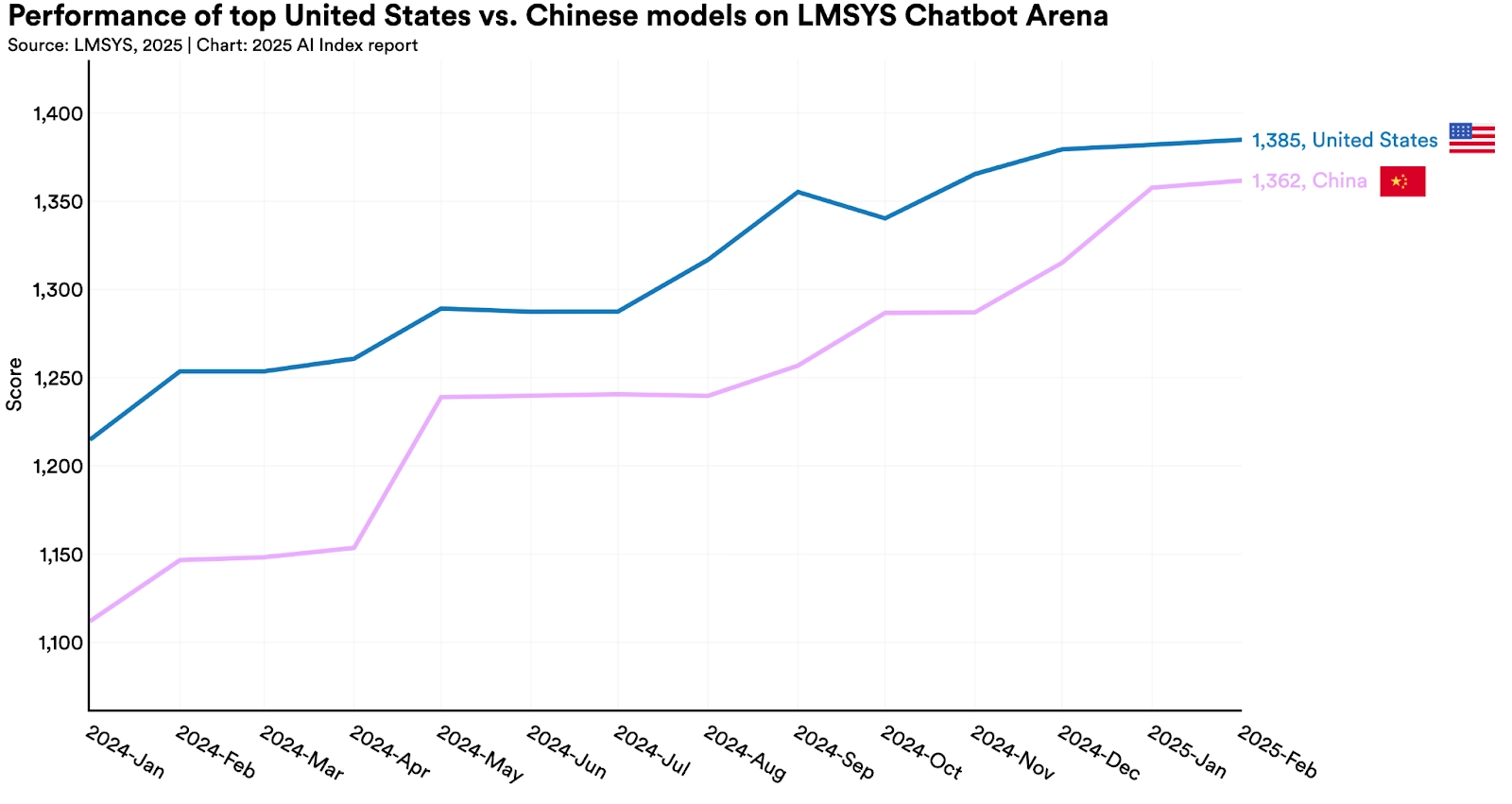

While the United States maintains its quantitative lead in AI model development (producing 40 notable models in 2024 compared to China's 15 and Europe's 3), the qualitative gap has nearly disappeared.

The performance difference between American and Chinese models on benchmarks like MMLU and HumanEval shrunk from double-digit percentage points in 2023 to near parity in 2024. China also continues to lead in AI research publications and patents.

This narrowing gap suggests we're entering an era of global AI competition rather than American dominance. For businesses and policymakers, this has several implications:

A more diverse ecosystem of AI providers and approaches

Increased pressure for international standards and governance

Regional differences in AI development philosophies and applications

The report notably doesn't address how geopolitical tensions might affect this technology race, but it's clear that no single country has an insurmountable lead in AI development.

The Dark Side: AI Incidents Reach Record Levels

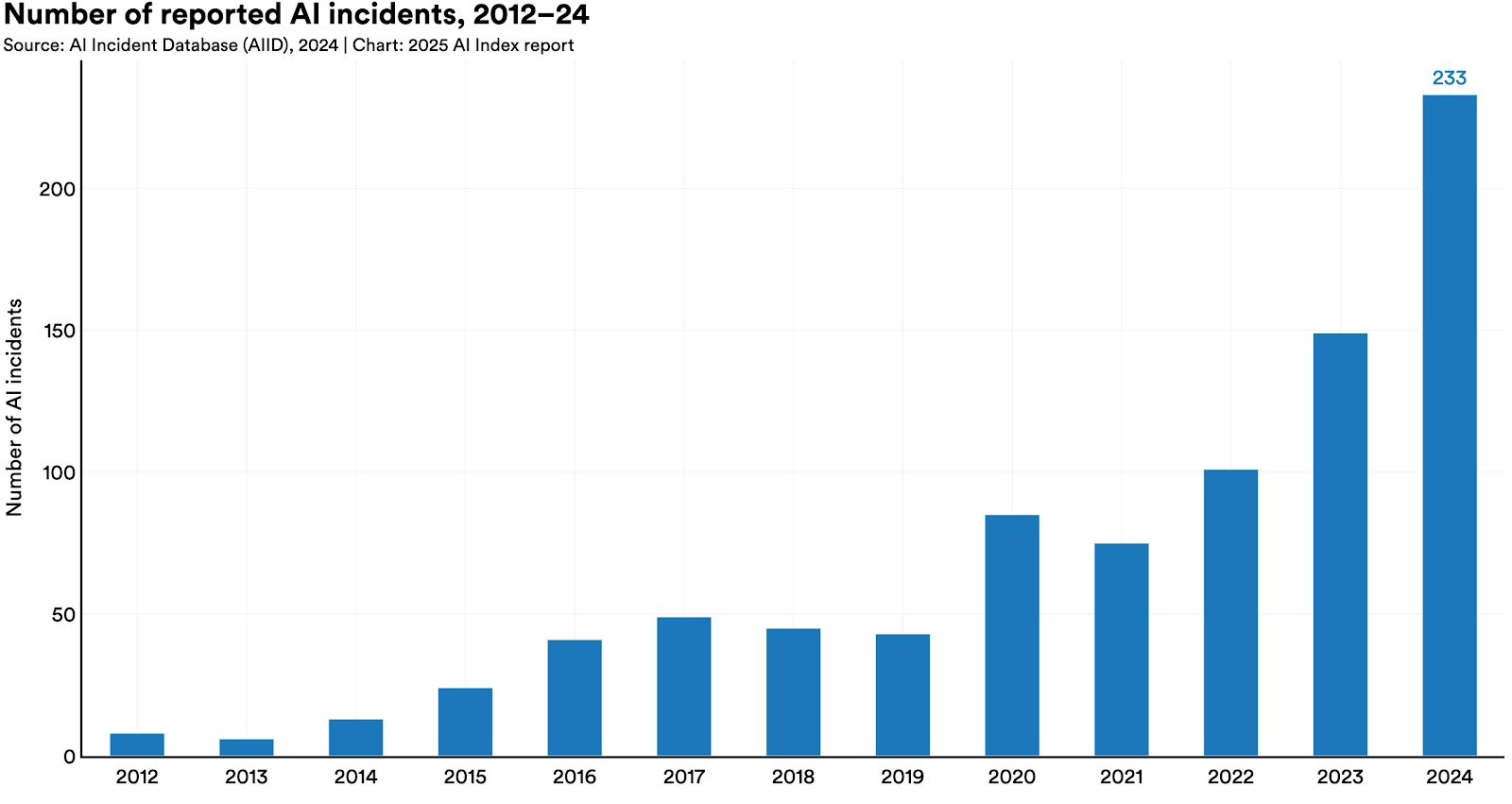

Not all the news is positive. The Stanford report highlights a concerning 56.4% year-over-year increase in documented AI incidents—reaching a record 233 cases in 2024.

These incidents range from deepfake intimate images to chatbots allegedly implicated in a teenager's suicide. While the report acknowledges this isn't a comprehensive accounting of all AI-related harms, the trend line is unmistakable and troubling.

As AI capabilities have become more powerful and accessible, the potential for misuse has grown proportionally. This underscores the urgent need for:

More robust safety mechanisms and guardrails in AI systems

Clearer legal frameworks for liability and accountability

Better education about AI risks for both developers and users

The industry's rapid progress in capabilities has outpaced our development of safeguards—a gap that needs urgent attention.

AI Agents: Almost Human, Sometimes Better

One of the most intriguing sections of the report examines the emergence of AI agents—systems that can autonomously perform complex tasks on behalf of users.

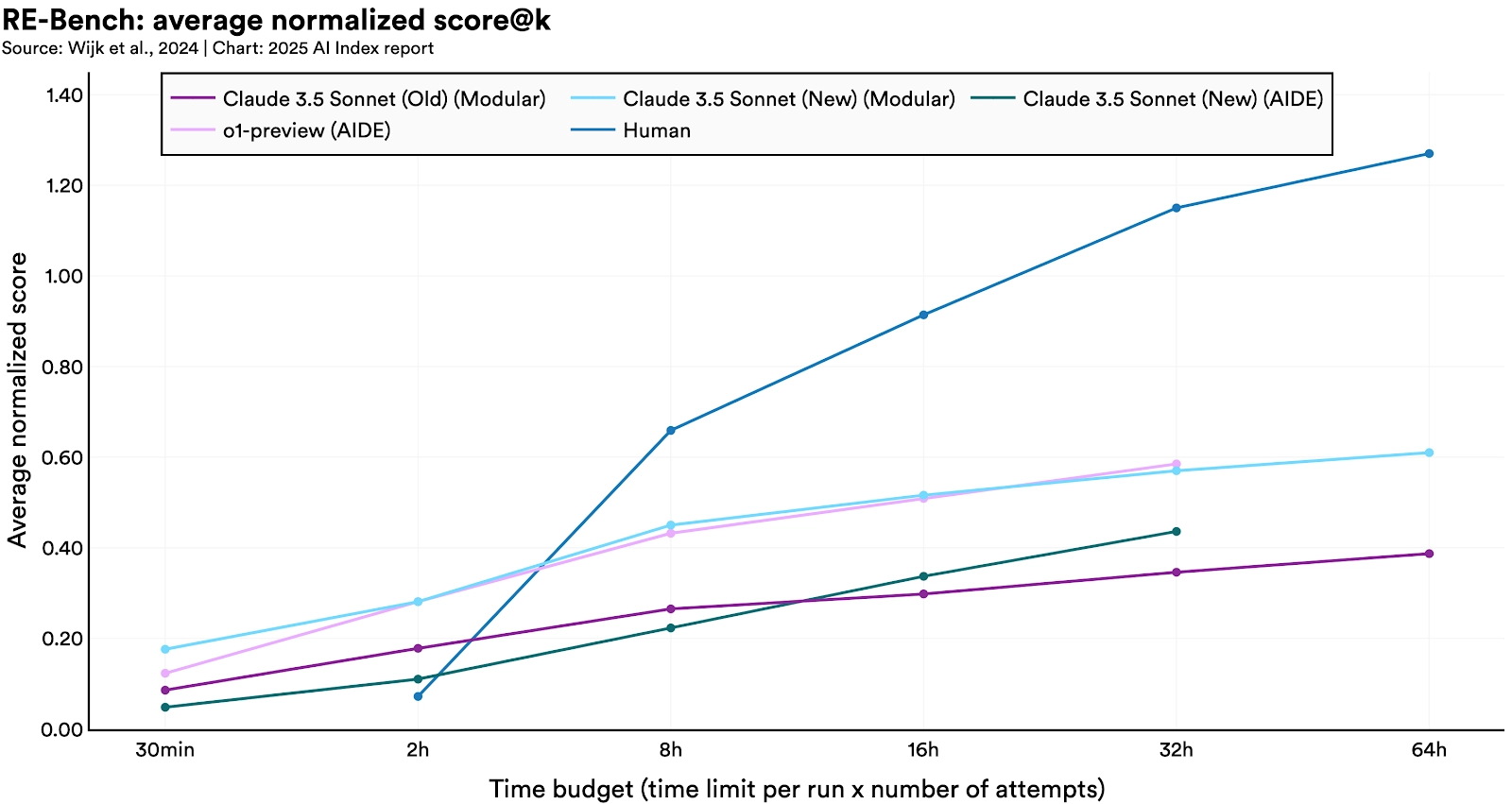

The introduction of RE-Bench in 2024 provides the first rigorous benchmark for evaluating these systems. The findings are revealing: in short time-horizon tasks (under two hours), top AI systems outperform human experts by a factor of four. However, humans still maintain an advantage in longer-duration tasks, outscoring AI 2-to-1 in 32-hour scenarios.

This suggests we're entering an era where AI agents excel at specific, well-defined tasks with clear parameters, while humans retain advantages in scenarios requiring extended reasoning, adaptation, and judgment.

For businesses, this points toward a future of human-AI collaboration rather than wholesale replacement, with each bringing complementary strengths to complex problems.

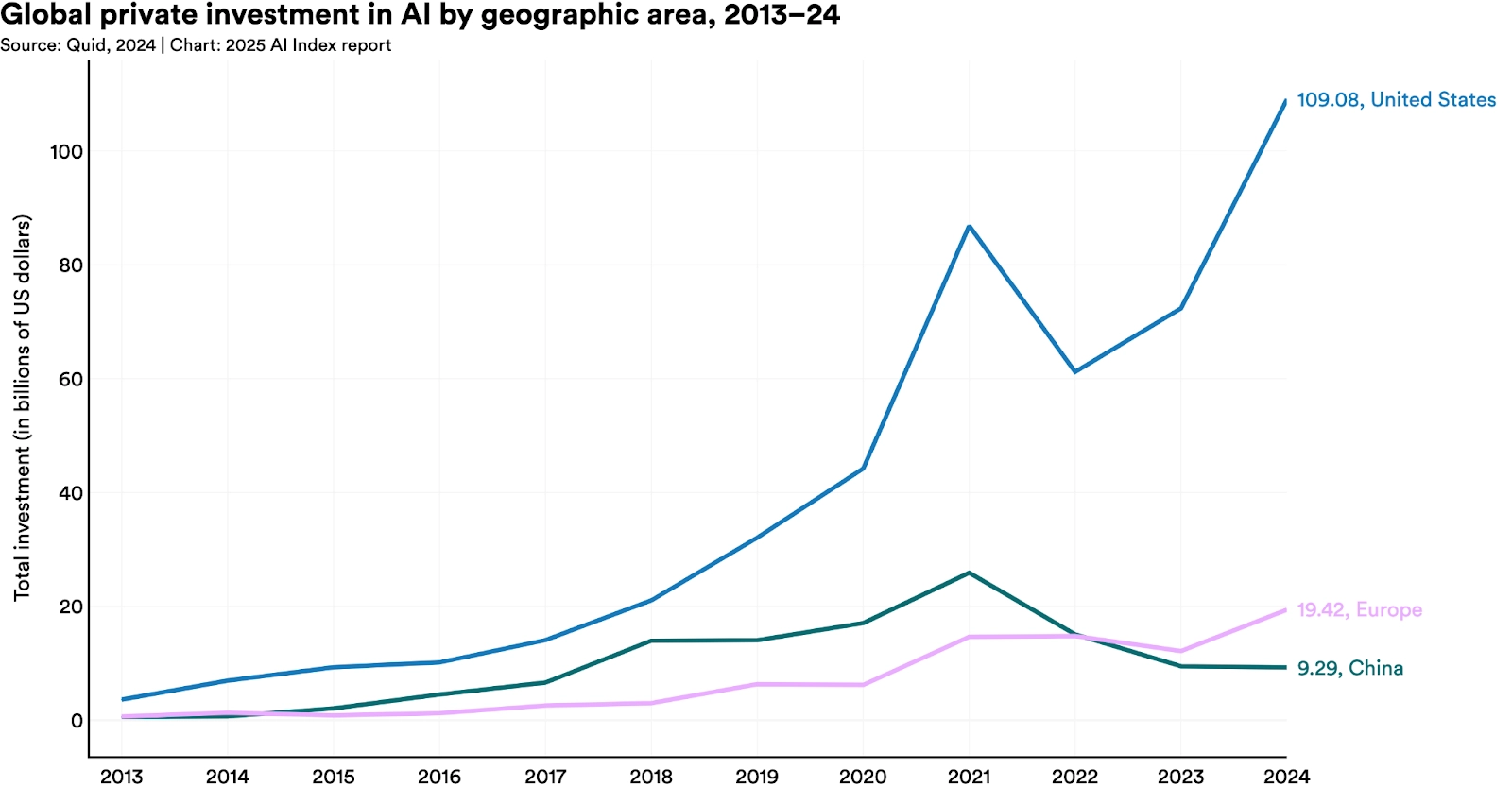

Follow the Money: U.S. Dominates AI Investment

If investment is a leading indicator of future innovation, the United States has positioned itself for continued AI leadership. U.S. private AI investment reached a staggering $109 billion in 2024—nearly 12 times higher than China's $9.3 billion and 24 times the UK's $4.5 billion.

The gap in generative AI investment is particularly striking, with U.S. funding exceeding the combined European Union and UK total by $25.5 billion, up from a $21.1 billion difference in 2023.

This concentration of capital creates both opportunities and challenges:

American AI companies enjoy unparalleled resources for R&D and scaling

Other regions risk falling further behind in commercializing AI innovations

The global AI landscape may become increasingly dominated by U.S.-based platforms and standards

How other nations respond to this investment gap will significantly shape the global AI ecosystem in the coming years.

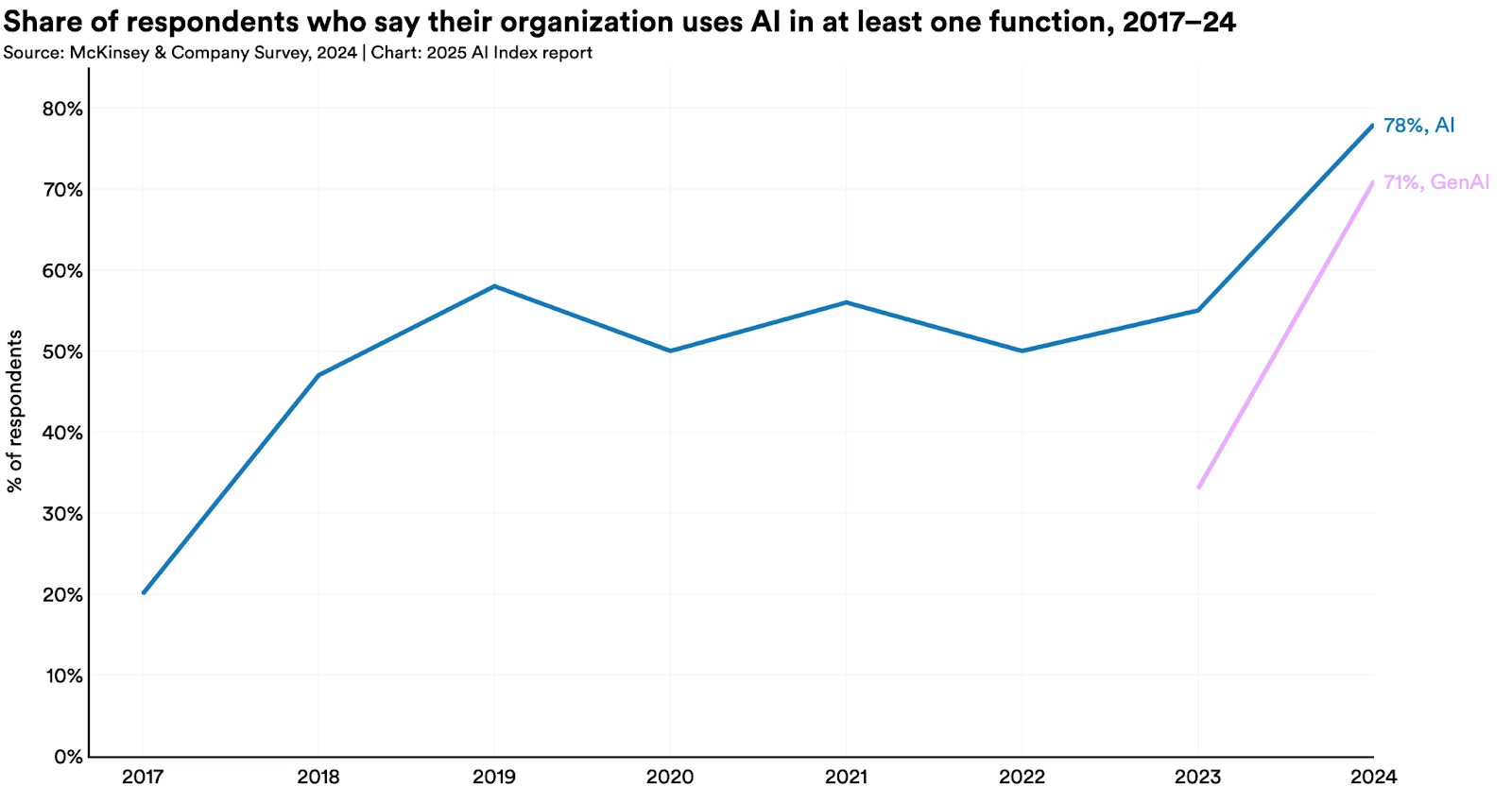

From Experimentation to Implementation: AI Goes Mainstream

Perhaps the clearest sign of AI's maturation is its rapid adoption across businesses. The proportion of survey respondents reporting AI use in their organizations jumped from 55% in 2023 to 78% in 2024.

Even more dramatically, the number reporting generative AI use in at least one business function more than doubled—from 33% to 71% in a single year. This shift from experimental adoption to operational implementation represents a crucial inflection point. AI is quickly transitioning from a speculative technology to an essential business tool across sectors. Companies that haven't begun serious AI integration efforts may soon find themselves at a significant competitive disadvantage.

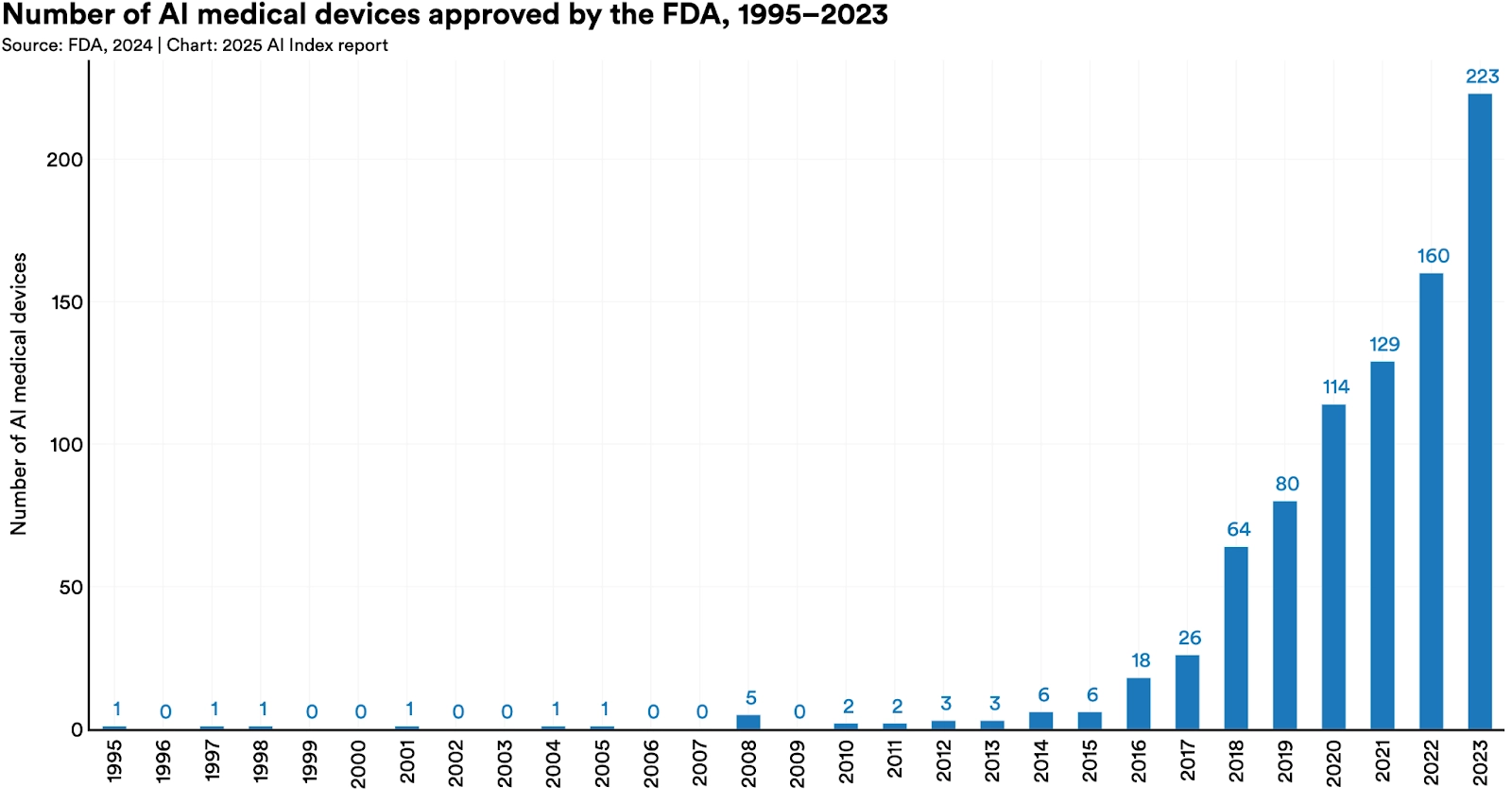

Healthcare's AI Revolution Accelerates

Few sectors demonstrate AI's growing real-world impact more clearly than healthcare. The FDA authorized its first AI-enabled medical device in 1995, and by 2015, only six such devices had received approval.

The landscape today is radically different—223 AI-enabled medical devices received FDA authorization by 2023. This exponential growth reflects both technological maturation and regulatory adaptation.

For patients and healthcare providers, this means:

More accurate diagnostics through AI-assisted imaging analysis

Enhanced monitoring of chronic conditions

Potential for more personalized treatment recommendations

The healthcare AI boom also highlights how sector-specific regulation can enable responsible innovation—a model other industries might consider following.

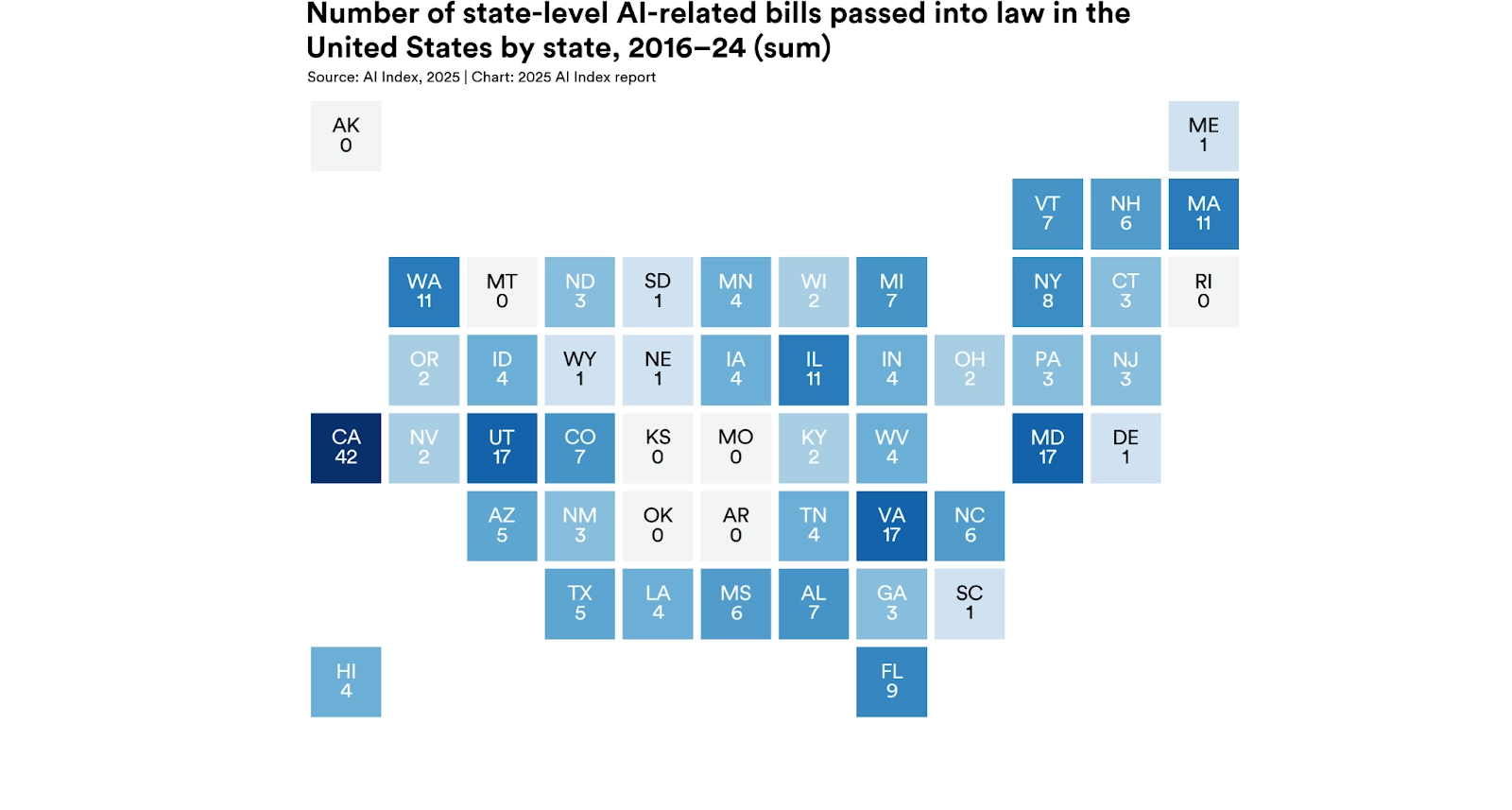

The Regulatory Response: States Lead While Federal Action Lags

As AI capabilities and incidents have grown, so too has regulatory attention—but not evenly across jurisdictions. In the United States, state-level initiatives have far outpaced federal action.

In 2016, only one state-level AI-related law existed. By 2023, that number had grown to 49, and in 2024 alone, it more than doubled to 131. Meanwhile, federal AI legislation, while increasingly proposed, rarely passes.

This regulatory patchwork creates significant challenges:

Companies must navigate inconsistent requirements across states

Some states may enact overly restrictive policies while others remain permissive

The lack of federal standards could inhibit nationwide AI deployment

The report suggests that without more coordinated federal action, the U.S. risks creating a fragmented regulatory environment that could ultimately disadvantage American AI development relative to countries with more cohesive approaches.

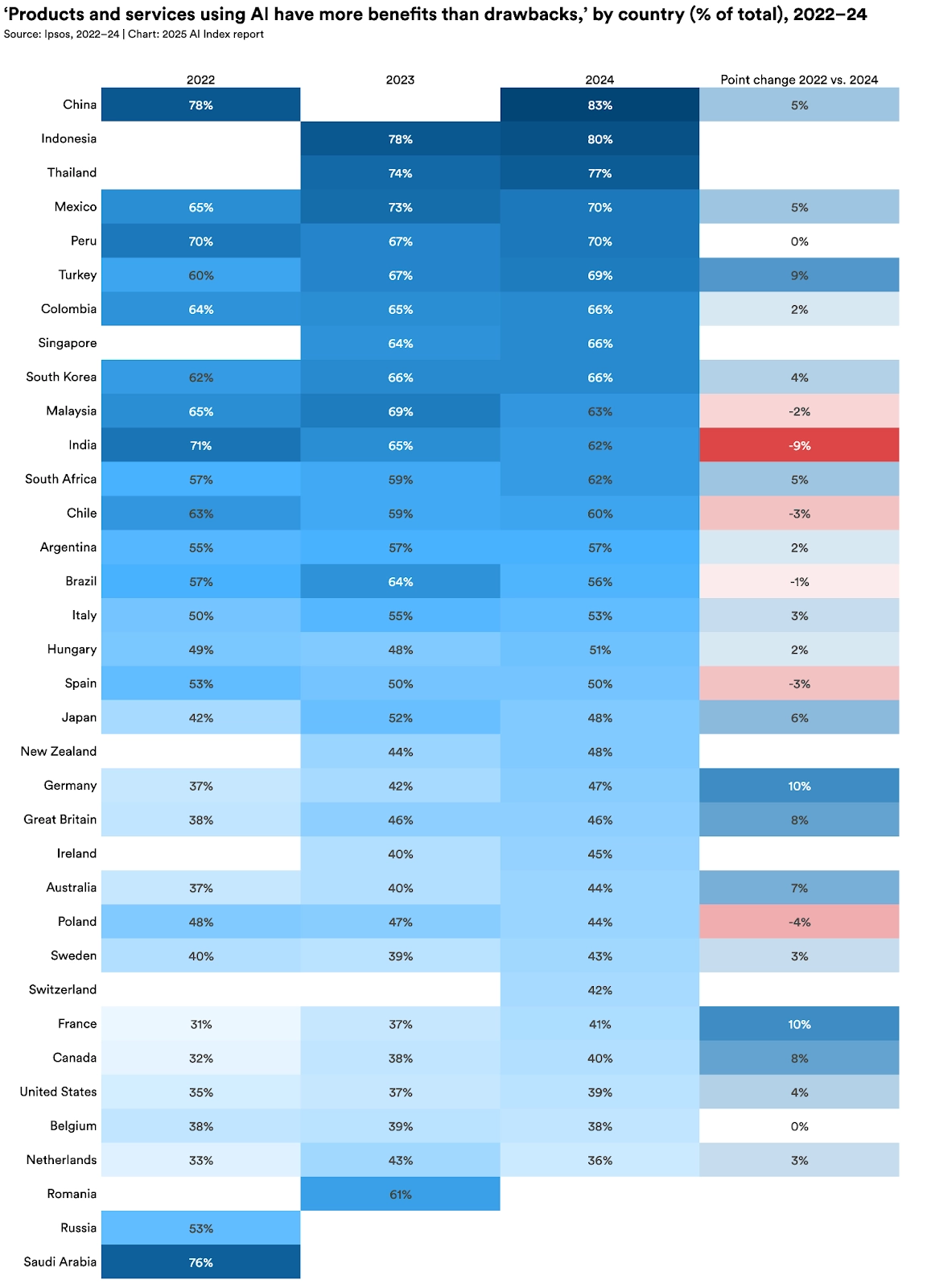

Cultural Attitudes: A Global Divide on AI Optimism

Perhaps the most interesting sociological finding in the report concerns global attitudes toward AI. While technological capabilities are converging across regions, perspectives on AI's impact remain sharply divided.

In Asian countries like China (83%), Indonesia (80%), and Thailand (77%), large majorities believe AI-powered products and services offer more benefits than drawbacks. In contrast, only a minority share this optimistic view in Canada (40%), the United States (39%), and the Netherlands (36%).

These attitudinal differences could influence everything from regulatory approaches to consumer adoption rates across regions. They may also reflect deeper cultural relationships with technology and automation that predate current AI developments.

For global companies deploying AI solutions, understanding and accounting for these regional differences will be crucial to successful implementation.

What Comes Next: Questions for 2026

As impressive as the 2025 AI Index is, it also raises important questions about where the field is heading:

Will the trend toward smaller, more efficient models continue, or are we approaching fundamental limits?

Can the industry address the rising tide of AI incidents without hampering innovation?

How will regional regulatory differences shape global AI development and deployment?

Will AI optimization finally deliver on the promise of edge AI running primarily on local devices rather than in the cloud?

Can the benefits of AI advancement be more equitably distributed across society?

What stands out most in this year's report is the sense of an industry in transition—from proof-of-concept to practical application, from quantity to quality, from centralized to distributed.

The technical achievements are impressive, but the real story is how quickly AI is becoming integrated into the fabric of business, healthcare, and daily life. The challenge ahead isn't primarily technological but social: ensuring that this powerful tool enhances human potential rather than diminishing it.